The first question a salesperson asks you isn't "what car are you looking for?"

It's "what monthly payment were you hoping for?"

I asked that question a thousand times. And every time, the customer thought I was being helpful. Trying to find something in their budget. Being a nice guy.

I wasn't.

I was setting a trap. And watching them walk right into it.

Here's what "monthly payment" talk is really designed to make you ignore. Once you see it, you can't unsee it.

What They Want You to Ignore 1: The Actual Price of the Car

This is the big one.

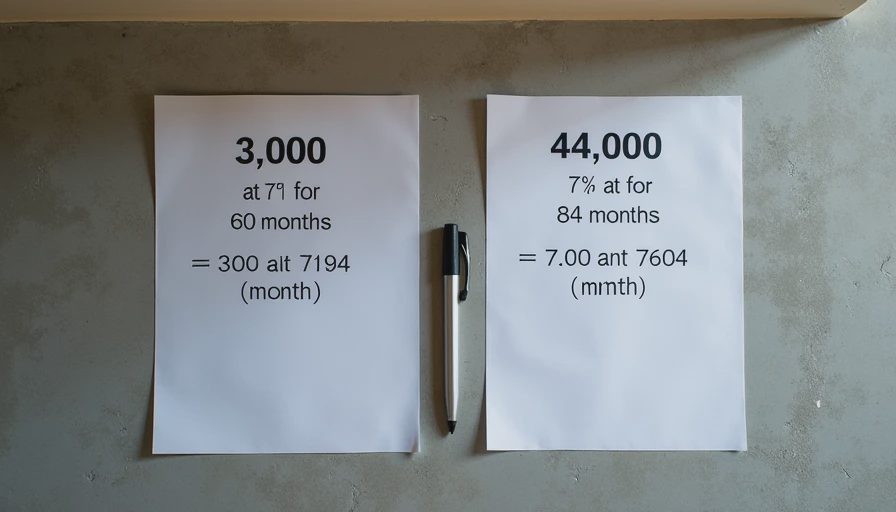

When you focus on the monthly payment, the price of the car becomes invisible. A 30,000 car and a30,000caranda40,000 car can have the exact same monthly payment if you stretch the loan long enough.

Let me show you the math:

Car A: 30,000 at 7% for 60 months =30,000at7594/month

Car B: 40,000 at 7% for 84 months =40,000at7604/month

Ten dollars more per month. For a car that costs ten thousand dollars more.

See the problem?

The salesperson isn't lying to you. They're just letting you lie to yourself. You said you wanted a 600 payment.

What to do instead: Refuse to talk monthly payment. Talk out-the-door price. That's the only number that matters.

What They Want You to Ignore 2: The Length of the Loan

Sixty months used to be standard. Then seventy-two. Now I regularly see eighty-four and even ninety-six month loans.

That's eight years. Eight years of payments on a car.

Here's what happens on a long loan:

You pay thousands more in interest

You're upside down (owe more than it's worth) for years

You can't trade the car without rolling negative equity into the next loan

You're still paying for the car after the warranty expires

What to do instead: Ask for the 60-month payment. If you can't afford it, you can't afford the car. Find something cheaper.

What They Want You to Ignore 3: The Interest Rate

Low monthly payments can hide a terrible interest rate.

A 35,000 car at 4% for 72 months is35,000carat4548/month. Same car at 10% is $648/month. That's a hundred dollar difference. Same car. Same loan length. Just a different rate.

But if you're only looking at the payment, you might not notice you're getting crushed on interest.

What to do instead: Get your financing squared away before you walk into the dealership. Credit union. Bank. Online lender. Walk in with a pre-approval letter. Then let the dealer try to beat the rate. If they can't, use your own.

What They Want You to Ignore #5: What You're Giving Up

Every dollar you spend on a car payment is a dollar you can't spend on anything else.

What else could you do with $36,000?

A year of daycare

A decent family vacation every year

Home improvements

Saving for college

Paying down other debt

When you focus only on the monthly number, you lose sight of what that money represents. It's not just a payment. It's your life.

What to do instead: Calculate the total five-year cost of any car you're considering. Payment times months, plus down payment, plus estimated maintenance. That's what you're actually spending.

The Bottom Line

The monthly payment question isn't about helping you.

It's about getting you to ignore:

The actual price of the car

How long you'll be paying for it

What interest rate you're getting

The cost of hidden add-ons

What else you could do with that money

Walk into the dealership knowing this. When they ask "what monthly payment were you hoping for?" say this:

"Let's talk about the out-the-door price first. I'll figure out the payment myself."

Watch how fast the conversation changes.

Because once you stop looking at the monthly fog, you can actually see the deal.

If the deal sounds clean, look for where they buried the dirt.